Listen to the article

Tokenization does not automatically make hard-to-trade assets liquid, industry executives said at Paris Blockchain Week, pushing back on the idea that putting private credit, real estate or other illiquid products onchain will by itself create active secondary markets.

Speaking during a panel moderated by Cointelegraph CEO Yana Prikhodchenko, Oya Celiktemur, Ondo Finance sales director for Europe, the Middle East and Africa (EMEA), said there is still a misconception that tokenizing illiquid assets can make them easier to trade.

“I think there’s still this idea that tokenizing something illiquid will somehow magically make it a liquid asset, which is just not true,” said Celiktemur. She added that assets like real estate and private credit “were never that liquid” to begin with.

Francesco Ranieri Fabracci, head of tokenization expansion at Tether, made a similar point. “It’s not that if you put an asset onchain, it will be liquid,” he said, arguing that only a narrower set of instruments, including bonds, money market funds and stablecoins, are likely to achieve consistent liquidity in tokenized markets.

The discussion comes as the tokenized real-world asset (RWA) sector continues to expand, shifting attention from issuance growth toward whether tokenized products can achieve meaningful activity and move beyond limited distribution channels.

Tokenized RWA market grows, but remains concentrated

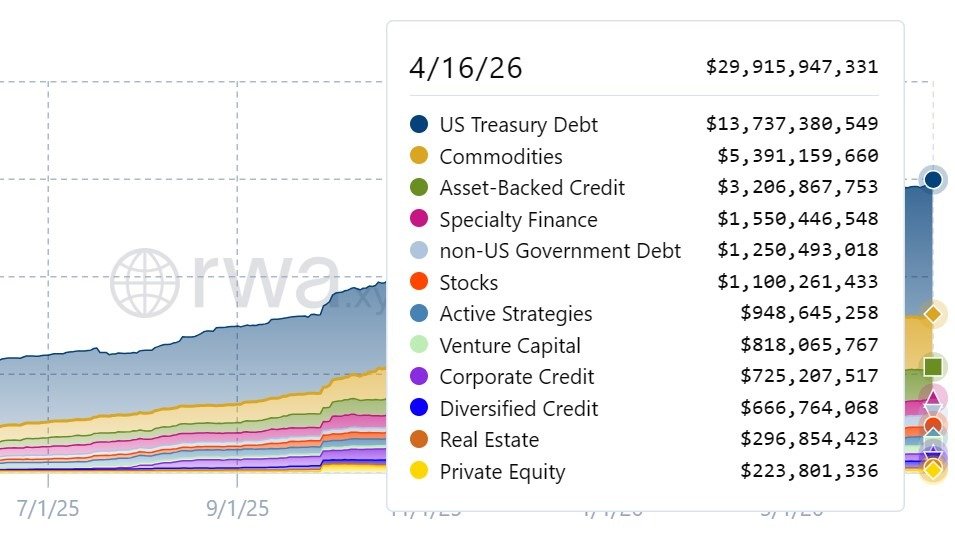

Data from RWA anayltics platform RWA.xyz shows the tokenized RWA market expanded from $8.8 billion on April 16, 2025, to roughly $29.9 billion on April 16, 2026, more than tripling in size in one year.

The growth was led by relatively standardized and widely traded assets. Tokenized US Treasury Debt and commodities accounted for a large share of the market throughout the year.

Related: French minister says new measures are coming after crypto kidnappings

By contrast, categories typically associated with lower liquidity remained comparatively smaller despite strong percentage growth. Tokenized real estate increased from about $35 million to $296 million, while private equity rose from nearly $60 million to $223 million.

Other segments, including asset-backed credit and corporate credit, also expanded sharply in absolute terms, indicating rising issuance across a broader range of instruments.

But market value alone does not prove liquidity. Outstanding value can rise because more assets are issued, even if secondary market trading remains thin.

Magazine: Singapore isn’t a ‘crypto hub’ — it’s something better: StraitsX CEO

Read the full article here

Fact Checker

Verify the accuracy of this article using AI-powered analysis and real-time sources.